🎧 Related Podcast Episode

Executive Summary

The global insurance landscape in 2026 is characterized by a shift from reactive financial protection to a proactive, technology-mandated resilience model. Organizations are navigating a high-stakes environment where cyber risk has ascended to a board-level priority, driven by the weaponization of generative artificial intelligence (AI), systemic cloud dependencies, and a “regulatory minefield” of data privacy laws.

Critical Takeaways:

- Market Dynamics: The global cyber insurance market is valued at approximately USD 33.05 billion in 2026, with a projected CAGR of 27% through 2034. While currently a “buyer-friendly” market, signs of tightening are emerging due to increased ransomware frequency and poor loss development.

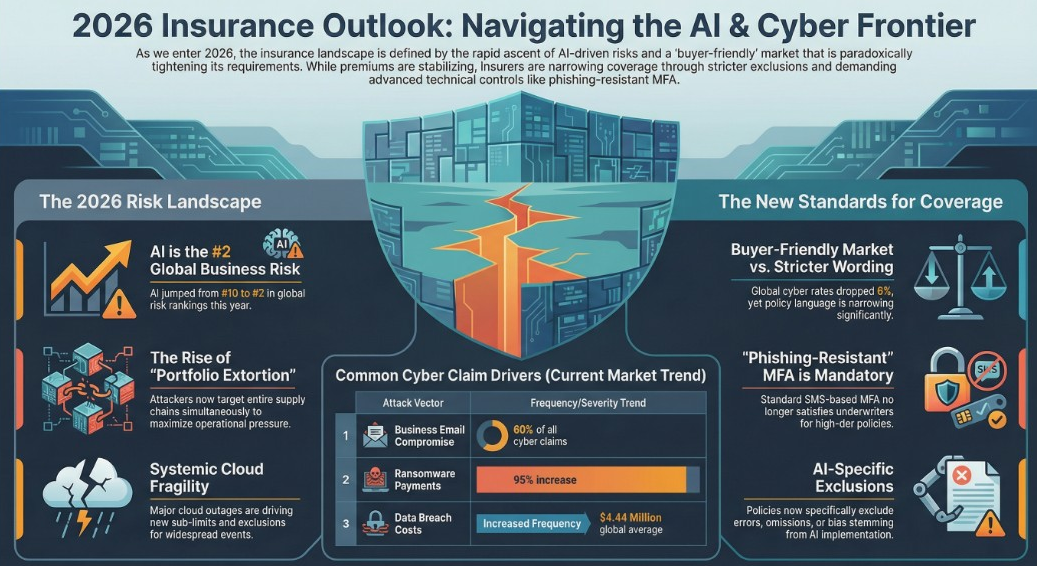

- AI-Amplified Threats: AI is a dual-edged catalyst, facilitating autonomous “agentic” attacks, hyper-personalized social engineering, and training data poisoning. Conversely, 94% of organizations recognize AI’s role in transformative defense.

- Mandatory Technical Controls: Insurers have transitioned from subjective surveys to data-driven audits. Phishing-resistant Multi-Factor Authentication (MFA) and Zero Trust Architecture are now non-negotiable prerequisites for high-tier coverage.

- Regulatory Intensity: 2026 marks “Phase Two” of the EU AI Act and the implementation of significant U.S. state-level AI regulations (CA, CO, NY). In healthcare, the updated HIPAA Security Rule mandates absolute encryption for all electronic Protected Health Information (ePHI).

- Social Inflation: Sky-high “nuclear verdicts” exceeding $10 million are driving social inflation, pushing liability premiums upward and challenging the predictability of legal risks.

1. The 2026 Global Insurance Market Environment

The 2026 market represents a critical inflection point where insurance providers no longer just transfer risk but mandate security maturity.

Market Trajectory and Economic Indicators

The market has entered a state of “disciplined underwriting.” While capacity is high, insurers are facing thin margins, particularly in the U.S., where intense competition meets rising loss severity.

|

Metric |

2026 Projected Status | |

Global Market Valuation |

~USD 33.05 Billion | |

North American Market Share |

~37% | |

Growth Drivers |

Regulatory mandates, AI risks, and cloud centralization | |

Pricing Trend |

Softened rates starting to stabilize/tighten |

Social Inflation and Escalating Jury Awards

Social inflation remains a primary cost driver. Shifting juror attitudes and third-party lawsuit funding have led to emotional, high-payout “nuclear verdicts.”

- Target Industries: Healthcare, automotive, and manufacturing are most vulnerable.

- Mitigation: Insurers are increasingly using AI to forecast legal risks, while some states weigh legislative reforms to curb excessive awards.

2. The AI Risk and Regulatory Frontier

In 2026, the “regulatory honeymoon” for AI is over. Organizations face a fragmented compliance landscape that treats AI data governance as a strategic imperative.

Global Regulatory Mandates

-

EU AI Act (Phase Two): By August 2, 2026, companies must comply with transparency requirements for “high-risk” systems (critical infrastructure, employment, healthcare). A new Code of Practice for labeling AI-generated content is expected by June 2026.

-

U.S. State Laws: California, Colorado, and New York have enacted laws covering automated decision-making.

- Colorado AI Act (Effective June 30, 2026): Requires risk management programs and measures to prevent algorithmic discrimination.

- California AB 2013: Mandates disclosure of datasets used to train generative AI.

-

Enforcement: State Attorneys General have formed a 42-state coalition to hunt for AI violations, emphasizing that “buying from a vendor” is not a defense for harmful AI outcomes.

AI-Driven Cyber Threats

Threat actors utilize AI to scale “asymmetrical warfare” against corporations.

- Agentic AI Breaches: Autonomous AI agents executing multi-stage campaigns without human intervention.

- Model Poisoning: Altering as little as 0.1% of training data to cause targeted misclassification.

- Synthetic Insider Threats: AI agents mimicking employee voice and linguistic patterns to bypass platforms.

3. Cyber Insurance: Provider Benchmarking and Costs

Cyber insurance has bifurcated into specialty categories, with providers prioritizing different risk profiles.

Leading Carriers and Specializations

Based on 2026 market analysis, three providers lead the industry in small-to-midmarket (SMB) effectiveness:

|

Provider |

Core Strength |

2026 Strategy | |

Chubb |

Best Overall |

Deep coverage, A++ rating, and 24/7 breach response. Offers personal cyber plans. | |

Hiscox |

Cyber Crime |

Market leader in social engineering and funds transfer fraud (FTF) protection. | |

Coalition |

Risk Management |

“Active Insurance” model; includes continuous scanning and threat alerts. |

- Large Enterprise Leaders: AIG (offering limits up to $100M), Zurich, and Tokio Marine are preferred for Fortune 500 and multinational corporations.

- Average Costs: For SMBs, premiums average $145 per month. However, tech-forward firms may pay more for “Active Insurance” models that include preventive tools.

4. Underwriting Innovations and Technical Eligibility

In 2026, the baseline for insurability is significantly higher. Insurance is no longer a safety net for poor security; it is a catalyst for security maturity.

Mandatory Technical Controls

Organizations failing to meet these technical “non-negotiables” face coverage denial or prohibitive premiums:

- Phishing-Resistant MFA: Traditional SMS or push-based MFA is no longer sufficient for high-tier policies. Carriers now mandate hardware security keys (FIDO2) or biometrics.

- Zero Trust Architecture: Identity is the new perimeter. Insurers require evidence of least-privilege access and microsegmentation.

- Endpoint Detection and Response (EDR): 24/7 active monitoring and automated isolation of threats are standard requirements.

- Immutable Backups: Ransomware sublimits are often contingent on verified, air-gapped, and tested restoration capabilities.

Refined Exclusions and “Silent Cyber”

- LMA5567 War Exclusions: New clauses move away from “attribution” and focus on “impact.” Claims may be excluded if a cyber operation significantly impairs a state’s ability to function.

- Legacy Systems: Insurers increasingly exclude losses originating from end-of-life hardware or software that lacks modern encryption or MFA support.

- Systemic Cloud Failures: Due to single points of failure (AWS/Azure/GCP), many 2026 policies include sublimits or exclusions for multi-day outages of major cloud regions.

5. Critical Regulatory Updates: HIPAA and Healthcare

The healthcare sector faces a “schizophrenic” regulatory environment, with federal encouragement of AI adoption clashing with stringent state-level restrictions.

HIPAA Changes and Compliance

A major update to HIPAA is finalized for 2026, focusing on data access and security:

- Right of Access: The maximum timeframe for responding to patient records requests is reduced from 30 days to 15 days.

- Mandatory Encryption: Updated Security Rules mandate encryption for all ePHI at rest and in transit, utilizing AES-256 (symmetric) and TLS 1.3 (transit).

- Audit Revival: The Office for Civil Rights (OCR) has revived its proactive audit program, focusing on risk analysis and management.

- 42 CFR Part 2 Alignment: By February 16, 2026, substance use disorder (SUD) records must align more closely with HIPAA, allowing single patient consent for all future TPO (Treatment, Payment, Operations) uses.

6. Emerging Enterprise and Operational Risks

Beyond cyber, businesses must prepare for interconnected risks that can trigger chain reactions in 2026.

- Climate-Related Property Losses: Frequent hurricanes and wildfires are making property insurance unaffordable in high-risk regions. Some insurers have ceased offering coverage entirely, leading to the rise of parametric insurance, which pays out based on measurable triggers (e.g., wind speed) rather than damage assessments.

- Supply Chain and Distribution Failure: High-profile incidents (e.g., Change Healthcare, CrowdStrike) have exposed systemic business interruption risks. Third-party involvement accounted for 30% of all data breaches in 2025.

- Technology Debt: “Legacy systems” are harder to defend and serve as prime targets for AI-driven attacks. Insurers are increasingly viewing technology debt as a material liability that affects overall risk profiles.

7. Strategic Recommendations for Leadership

To thrive in the 2026 landscape, organizations should adopt a “resilience paradigm”:

- Reinvest Premium Savings: Use savings from the currently soft market to enhance controls and expand coverage limits rather than simply reducing spend.

- Adopt Phishing-Resistant MFA Everywhere: Applying hardware keys across email, VPNs, and service accounts is the single most effective way to ensure policy eligibility.

- Formalize Cyber Resilience as a KPI: Track and report on resilience metrics as a business imperative, using data-driven risk modeling to inform investment.

- Audit AI Governance: Document AI usage, data handling, and adversarial red-teaming to satisfy underwriters and regulators.

- Address Technology Debt: Isolate unsupported legacy systems through microsegmentation if they cannot be fully decommissioned.